The Value of your Money Purchase Account

Remember that the pension you receive is designed to be the Final Salary Pension, and so this is the pension that most members of the Scheme will receive. If you are instead paid a Money Purchase Pension, this page explains how the Money Purchase Account that pays for it is valued.

To find out more about the difference between the Final Salary and Money Purchase pensions see the page about Pensions and Lump Sums.

On your benefit statement we show you a Money Purchase Pension income based on the current money in your Money Purchase Account and assuming you are age 65.

Every month that you made a contribution to your pension, you paid 3.5% of your pensionable monthly earnings into your Money Purchase Account. Your employer matched this by also paying the equivalent of 3.5% of your pensionable monthly earnings into your Money Purchase Account.

(Members who paid contributions between October 2007 and March 2008 paid an additional 0.6% of pensionable monthly earnings, while those who paid contributions from April 2008 onwards paid an additional 1.3% of pensionable monthly earnings. If this applies to you, this additional contribution was not added to your Money Purchase Account, but is used, alongside additional Employer contributions, to help fund the automatic additional benefits that are not paid for by the Money Purchase Account – e.g. pension increases in retirement and contingent dependants’ benefits).

The money in your Account is invested in the Prudential With-profits Fund, so your money is pooled together with money from other people. The Fund is managed by Prudential, who puts the money into different types of investment, such as equities (company shares), property, bonds and cash.

The costs of running the With-profits Fund incurred by the Prudential are deducted and what is left over (the profit) is available to be paid to you and all the other investors - you get your share of the profits in the form of Annual Bonuses added to your Account. Once an Annual Bonus has been declared and applied to the money in your Account it can never be removed.

The Prudential tries to avoid big changes in the size of the bonuses from one year to the next. It does this by holding back some of the profits from good years to boost the profits in bad years – this process is called ‘smoothing’.

As a result of the smoothing you might also get a Terminal Bonus when you come to retire; it is awarded at the discretion of Prudential and they are at liberty to reduce it or even remove it entirely.

This why we tell you what the Terminal Bonus part of your Account is worth on your benefit statement. Knowing this you can envisage how much your income would reduce by if Prudential did not award it; e.g. if your Terminal Bonus makes up half your Account, then without it you would get half the income we have calculated.

(It is worth noting that even though in some years when there has been very poor investment performance the Prudential have reduced the Terminal Bonus applicable to the Scheme, they have never yet removed it altogether. The Scheme has been running since 1974).

The Trustees may be able to claim compensation under the Financial Services Compensation Scheme if Prudential are unable to meet their liabilities to the Trustees. The current level of compensation available is 90% of the claim with no upper limit. Prudential Assurance Company Ltd, the money purchase fund investment manager, is a subsidiary of Prudential PLC, one of the UK's largest insurance companies, and is authorised and regulated by the Financial Conduct Authority.

The Value of your AVC Account

If you have made additional voluntary contributions to Prudential, received an augmentation payment from your Employer or transferred-in a pension from another pension arrangement to your Pension, this money has been added to a separate AVC Account that is invested with Prudential and is given bonuses in exactly the same way as your Money Purchase Account.

If you made additional voluntary contributions to Legal & General, Utmost Life (Equitable Life as was) or Clerical Medical, this money is now invested with the Aviva Master Trust. We do not include this money on our calculations. Aviva may provide you with a statement of these funds and you can find out more about the Aviva Master Trust here.

Prudential Statutory Money Purchase Illustration (SMPI)

Special rules apply to “money purchase” pensions, and so we are obliged by legislation to provide you with an SMPI of the possible income from the money in your Money Purchase Account plus your Prudential AVC Account, if you have one. The SMPI is calculated for us by Prudential according to the strict rules set out in the legislation.

The SMPI has not been calculated using the basis prescribed by the Financial Services Authority. If you obtain illustrations from another pension arrangement you should consider whether or not they have been prepared on a similar basis to this one.

The SMPI calculation starts with an amount of money, forecasts how much that will grow to between now and age 65, reduces that forecasted amount to take account of inflation between now and age 65, then calculates an income in today’s money based on further assumptions about what the money has to pay for.

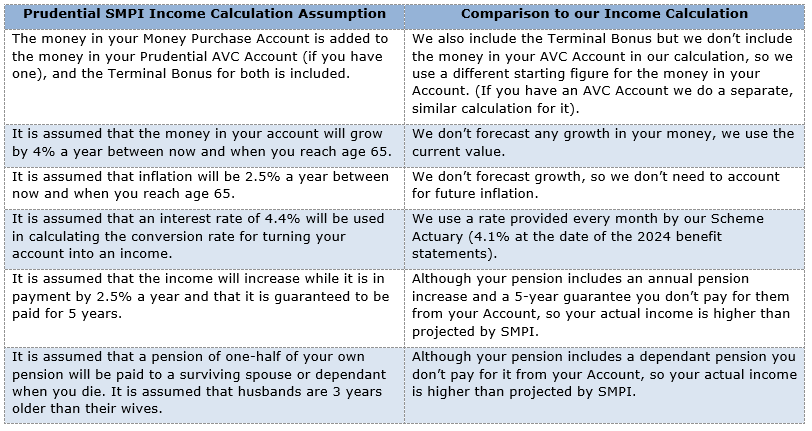

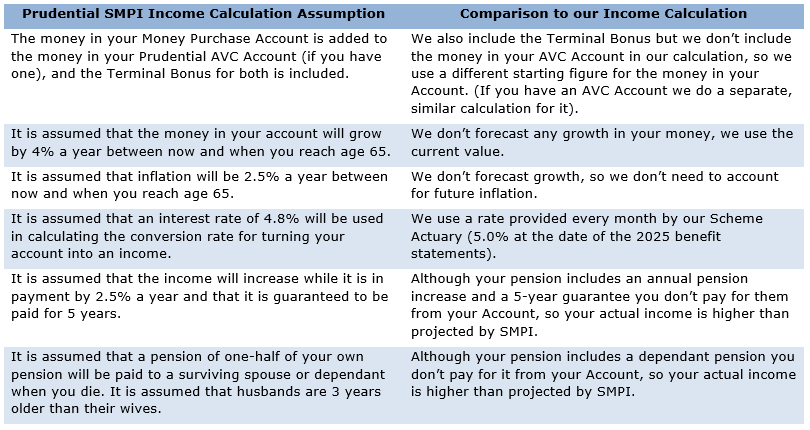

It is not the same calculation as the one we use for actually calculating your Money Purchase Pension income and it gives a different figure. The assumptions used for the SMPI income calculation (as at 1st April 2025) are as follows, along with a comparison to how we calculate your income.

Assumptions Used on Previous Benefit Statements

The assumptions used by Prudential to calculate the SMPI may change every year.

Those used on the benefit statements issued at 1st April 2024 were as follows.