Final Salary Pension Calculation

Your Final Salary Pension is calculated from the salary you were being paid by Which? when you left the Scheme(1) and your length of service in the Scheme. The calculation works out the pension to be paid to you on your 65th birthday, in accordance with the Scheme Rules.

On your benefit statement, the Final Salary Pension at the date you left the Scheme(1) has been revalued by the inflation in prices since, so that the income is expressed in today’s money terms.

This revaluation by inflation only applies to the date when you reach age 65. If you are over 65, the Final Salary Pension has been uplifted for late retirement.

Actually the calculation is much more complicated than this, because the meanings of ‘salary’ and ‘service’ have to be carefully defined for precision, fairness and clarity.

(1)(Or switched to the now closed DC Section of the Scheme).

Calculation in Detail

The calculation is as follows:

(1/90 x Final Pensionable Salary below the Scheme Specific UEL x Pensionable Service) +

(1/60 x Final Pensionable Salary above the Scheme Specific UEL x Pensionable Service)

(If you have service before 1st April 1988, the fraction applied to that period of service is 1/100 instead of 1/90).

Your Final Pensionable Salary is calculated from the contributions you made in your last ten years of service.

(We don’t simply use the salary on your payslip because this could include payments for aspects of your work that were excluded from your pension for legislative, tax or contractual reasons - such as P11D benefits, commission payments, car allowance, bonus payments etc).

We don’t just use the contributions as paid, we first make three types of calculations on them:

- If you were working part-time for a period, the contributions paid in that period are scaled-up as though you were working full-time. (Any part-time service is accounted for in the calculation of your period of service).

- In order to take inflation into account, each month’s scaled-up contribution is revalued by the change in prices between the month it was paid and the date you left the Scheme(1), using the Retail Prices Index.

- And finally so as to use earnings that are more representative of your last ten years of service, we look at each year’s worth of inflation-revalued contributions and use the average annual earnings in the highest three consecutive years within the last ten years. For most people this works out as the average of their last three years’ revalued contributions, but if your salary increases did not keep pace with inflation it may work out to be an earlier three-year period.

The Scheme Specific UEL is a monetary value equal to the Upper Earnings Limit - as defined by the Department of Work and Pensions - that was in effect on 1 April 2008, increased by the yearly change in the Retail Prices Index until the date you left the Scheme(1).

The reason we use the Upper Earnings Limit (UEL) in our calculation is because historically the State Pension (the pension paid to you by the government) included only earnings up to the UEL. This meant that earnings above the UEL did not contribute to the State Pension. Under the Scheme Rules the member’s earnings above this limit receive more from the Scheme.

Hence in the calculation the part of your Final Pensionable Salary above the Scheme Specific UEL is divided by 60 rather than 90.

Your Pensionable Service is calculated as complete years and complete months of service in the Scheme.

If you joined employment part way thorough a month, your pensionable service could begin on the first day of the following month. If you left employment part way through a month, your pensionable service would end on the last day of the prior month.

If you had periods of part time service or unpaid leave, your pensionable service is reduced to take account of this. For example if you worked four days per week for five years, your pensionable service would be calculated as four complete years.

Revaluation by Inflation until Age 65

To take account of inflation (the increase in prices of consumer goods over time) since the date you left the Scheme(1), the Final Salary Pension is revalued for each complete year that elapses until your 65th birthday. The amount of the revaluation is defined by legislation and is based on annual changes in RPI up to the year 2010, and then annual changes in CPI up to a cap of 5% since then.

If you are over 65, you can find out about Late Retirement below.

(1)(Or switched to the now closed DC Section of the Scheme).

Money Purchase Pension Calculation

Your Money Purchase Pension is calculated from the amount of money in your Money Purchase Account, using a conversion rate that is calculated for us by the Scheme Actuary.

On your benefit statement, the conversion rate that has been used assumes current market conditions and an age of 65, so that the income is expressed in "today’s money" terms and is comparable to the Final Salary Pension.

Calculation in Detail

The money in your Money Purchase Account is made up of contributions you and the employer made on your behalf plus an Annual Bonus that is awarded by Prudential for every year it is invested. Once an Annual Bonus has been applied to the money in your Account it can never be removed.

In addition you might also get a Terminal Bonus when you come to retire.

Although we include the Terminal Bonus in our calculation of your possible income, it is awarded at the discretion of Prudential and they are at liberty to reduce it or even remove it entirely; if they did so it would result in a lower income than we calculate.

The bonuses are calculated by Prudential from the investment performance of their With-profits Fund, hence the amount of money in your Account depends on the performance of the investments.

In order to convert your Account into a monthly income, a conversion rate is calculated for us by the Scheme Actuary with reference to age, the current money market conditions and current statistics about how long people live on average (longevity). Longevity depends upon gender. Because the conversion rate depends upon and is determined by current circumstances, it changes from month-to-month.

It is worth noting that the determination of this conversion rate doesn't take any account of the cost of providing pension increases and a spouse pension when you die, although these benefits are always automatically granted with your pension.

Hence it is a higher conversion rate than if these benefits were part of the calculation. In effect these benefits are not paid for by you out of your Account, they are paid for by the Scheme.

Find out more about how we value your Money Purchase Account here.

Aviva Master Trust, AVC, Augmentation and Transfer-in Pension Calculation

If you have

- made additional voluntary contributions (AVCs) to Prudential,

- received an augmentation payment from your Employer that was then invested with Prudential,

- or transferred-in a pension from another pension arrangement that was then invested with Prudential

this money has been added to a separate additional benefit account, which we simply refer to as your AVC Account.

This is invested with Prudential and is given bonuses in exactly the same way as your Money Purchase Account – see above.

On the benefit statement we show you how much income you could convert your AVC Account to, again based on a conversion rate calculated by the Scheme Actuary.

However unlike the conversion rate calculated to convert the Money Purchase Account to income, the cost of funding pension increases and a contingent spouse pension is used to determine the rate and so results in a lower conversion rate by comparison.

This means that if you want to take a tax-free cash lump sum from your Scheme pension at the point you retire, you might be better off if you use up your AVC Account towards this lump sum rather than for extra income.

Alternatively you may draw the money out of your AVC Account as a lump sum once you reach age 55(2).

When you come to retire or consider taking benefits, we will always illustrate to you the impact on your overall benefits of the different uses of your AVC Account.

Aviva Master Trust

If you saved AVCs with Legal & General, Clerical Medical or Utmost Life (Equitable Life as was), this money is now invested in the Aviva Master Trust, in a section known as the Consumers' Association Retirement Savings Plan, or CARSP.

To find out more about the Aviva Master Trust see here.

Aviva may provide you with an annual statement of your benefits in the Aviva Master Trust.

Apart from this difference in how your Aviva Master Trust money is invested, the rules for how you use the money are exactly the same.

Early and Late Retirement Calculation

In accordance with the Scheme Rules the calculation of the Final Salary Pension is to work out the income to start on your 65th birthday, your normal retirement age.

However, legislation allows you to take any retirement benefit from age 55(2). Hence if you wish to retire before your 65th birthday, your Final Salary Pension is reduced by an Early Retirement Factor.

(2)The government is changing this age. From 6th April 2028, you must be at least 57 years of age before you can take any pension benefits.

Early Retirement

If you wish to retire between your 55th and 65th birthdays, your Final Salary Pension is reduced by an Early Retirement Factor, which is calculated for us by the Scheme Actuary.

The principle behind this is that your pension income will be paid for the rest of your life, so if you take it earlier than age 65 it has to last you for longer hence the monthly income must be reduced. In this way, in principle the total money paid to you over your entire retirement is the same as if you had retired at age 65.

e.g. £7,500 per year paid to a member retiring at age 65 for 20 years adds up to a total payment of £150,000

(7,500 x 20 = 150,000).

If the same person retired 10 years earlier, the same £150,000 has to provide an income for 30 years, so the income should be reduced to £5,000

(5,000 x 30 = 150,000).

This is not exactly how the calculation is done, it is a simplification to illustrate the principle.

(If the Money Purchase Pension is paid to you before age 65, note that the conversion rate to calculate your income automatically takes account of your earlier age).

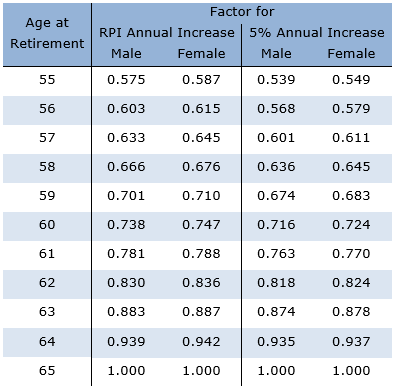

The true Early Retirement Factors that currently apply are in the table below. These are currently being reviewed quarterly.

The factors are different for men and women. This is because women are expected to live longer than men.

They are also different depending on whether your pension in payment receives annual increases fixed at 5% or annual increases calculated from the Retail Price Index. This is because the rate your pension increases by each year determines how much is paid in total over your entire retirement.

e.g. from the table below for a woman retiring with RPI increases on her 55th birthday, her income would be reduced by multiplying it by 0.587.

Early Retirement Factors from 19th August 2025

Late Retirement

If you retire after your 65th birthday, your Final Salary Pension is increased by a Late Retirement Uplift which is calculated for us by the Scheme Actuary.

The principle behind this is similar to above - your pension income will be paid for the rest of your life, so if you take it later than age 65 it doesn’t have to last you for as long hence the monthly income must be increased. In this way, in principle the total money paid to you over your entire retirement is the same as if you had retired at age 65.

You must take all your benefits before your 75th birthday.

For comparison, we also calculate what your revalued Final Salary Pension would be if we revalued by inflation from the date you left the Scheme(1) until your retirement date, in order to ensure that the Late Retirement Uplift calculation gives you at least that income.

(If the Money Purchase Pension is paid to you after age 65, the conversion rate to calculate your income automatically takes account of your later age).

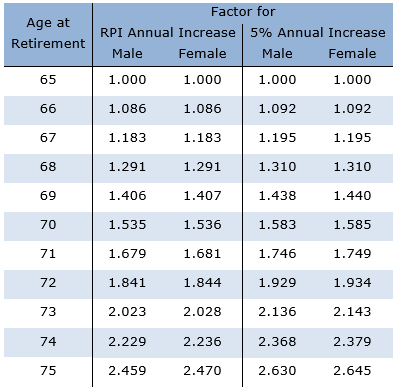

The true Late Retirement Factors that currently apply are in the table below. These are currently being reviewed quarterly.

The factors are different for men and women. This is because women are expected to live longer than men.

They are also different depending on whether your pension in payment receives annual increases fixed at 5% or annual increases calculated from the Retail Price Index. This is because the rate your pension increases by determines how much is paid in total over your entire retirement.

e.g. from the table below for a man retiring with 5% increases on his 75th birthday, his income would be increased by multiplying it by 2.630.

Late Retirement Factors from 19th August 2025

1(Or switched to the now closed DC Section of the Scheme).

Important Note

Pension benefits built up in the UK cannot legally be accessed before age 55 except in circumstances of ill health incapacity, and there are no legitimate loopholes that allow this.

The government is changing this age. From 6th April 2028, you must be at least 57 years of age before you can take any pension benefits.