Get 1-to-1 money guidance

Which? Money members can get impartial guidance from our experts, based on 350 years’ combined financial services experience.

Find out more

Faye was Headline Money Consumer Money Journalist of 2023 and a Wincott Award finalist in 2025. She's been investigating scams for nearly a decade.

A social media ‘finfluencer’ has been convicted of illegal promotions, while hundreds of others have been warned or taken offline, in the regulator's latest crackdown on illegal money content.

The UK’s Financial Conduct Authority (FCA) worked with 16 regulators as part of the co-ordinated action, including those in Australia, Canada, Qatar and the UAE.

In the UK, only authorised firms and people can promote investments or give financial advice. But social media sites are rife with illegal, misleading and low-quality money content.

Here Which? explains what the crackdown means, where the rules apply and how to find financial advice you can trust.

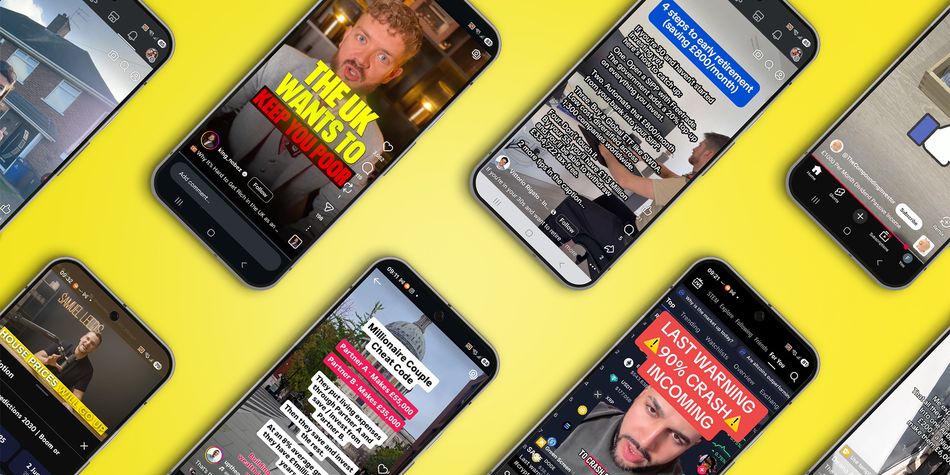

Financial influencers (often called ‘finfluencers’) are social media creators who share tips or opinions about money, including investing, property and building wealth.

Only authorised firms and individuals can promote investments or give financial advice in the UK, but social media is still awash with content that flouts the law.

Some creators do share useful information, but poor-quality posts are often presented in a polished and convincing way. This can lead you to make unsuitable financial decisions or even fall victim to scams.

The FCA’s latest ‘week of action’ highlights the scale of the problem. It identified more than 1,200 potentially illegal financial promotions and issued dozens of warnings to individuals and firms. It also requested the removal of more than 100 social media accounts.

In November 2025 we shared 8 examples of widely available finfluencer content with chartered financial planner Dr Robin Keyte for analysis.

They spanned investments, property, tax, crypto and general wealth-building tips.

Dr Keyte identified an array of serious problems including misleading statements, factual errors, incorrect assumptions and severely oversimplified claims.

And Which? felt one of the finfluencers strayed close to regulated activity by promoting a particular investment product and provider, despite not being authorised by the FCA – a concern we flagged to the regulator.

Your experience could help others avoid making costly mistakes. Email us at yourstory@which.co.uk

By law, only FCA-authorised people or firms can do the following:

Those who carry out these activities online without authority are breaking the law and can be prosecuted.

Many creators flout the law, and the FCA's crackdown focuses on this type of content. That's because it has enforcement powers, such as the ability to prosecute offenders.

However, many finfluencers avoid regulated activity and instead sell education and training courses or materials that purport to tell you how to pick your own investments to build wealth.

Such content can still be harmful and misleading, with some users persuaded to spend large sums on courses and seminars of dubious value.

Because this activity is unregulated, it falls largely to social media platforms to police it. Yet the sheer volume of it available online shows this isn't working.

For complex financial decisions, such as pensions, investments, inheritance planning or mortgages, consulting an independent, FCA-regulated financial adviser (IFA) or chartered financial planner is ideal.

You can use a comparison site such as unbiased.co.uk or vouchedfor.co.uk and filter the results based on expertise and customer reviews.

Charges will vary. With investments, it’s common to be charged a percentage of the investment. The average fee is 2.4%. With advice on other products (such as insurance or mortgages) you may be charged a flat fee or an hourly fee for the IFA’s time.

If you can’t afford an IFA, or for simpler financial decisions, impartial free guidance can be a good alternative. Instead of recommending a specific product, it gives you general information to help you narrow down your choices yourself.

MoneyHelper and Pension Wise (both at moneyhelper.org.uk) and Citizens Advice (citizensadvice.org.uk) all provide guidance. Which? Money members also have access to 1-to-1 appointments with our money experts.

You can check whether a person or firm is regulated – and any warnings about it – using the FCA's firm checker.

Which? Money members can get impartial guidance from our experts, based on 350 years’ combined financial services experience.

Find out more