Need home insurance?

Use our customer scores to help you choose a great deal at MoneySuperMarket

Compare dealsWhich? earns commission to fund its not-for-profit mission if you buy a product

By clicking a retailer link you consent to third-party cookies that track your onward journey. This enables W? to receive an affiliate commission if you make a purchase, which supports our mission to be the UK's consumer champion.

Dean is an award-winning personal finance writer who’s spent over 15 years helping consumers navigate the tangled and fascinating world of insurance.

We've partnered with MoneySuperMarket to help you compare a wide range of home insurance options in one place, with added insight from Which?

Get a quote with MoneySuperMarket and we'll highlight Which? Best Buys and Recommended Providers in your results.

This is a Which? exclusive, so you won't find our scores or expert analysis on other comparison sites.

We rated 134 elements of each policy, covering buildings, contents and admin points such as fees.

We asked 2,804 home insurance customers who made a claim within the past two years to score their insurer.

In this article

As well as home insurance, Aviva offers car insurance, private health insurance and travel insurance.

Its home insurance is underwritten by Aviva Insurance Limited. It sells one policy directly and others via comparison websites. For information, Aviva also owns Quote Me Happy.

Aviva offers three home insurance policies – Signature, Online and Premium – and we reviewed all three. We've also surveyed 424 Aviva customers who have recently made a home insurance claim.

Please note that the information in this article is for information purposes only and does not constitute advice. Please refer to the particular terms and conditions of an insurer before committing to any financial products.

Here's how Aviva scored in our latest survey.

See how this compares with the best home insurance, or read more about how we rate home insurance.

We reviewed three of Aviva's policies. Select a policy from our table to see what it offers and how we rated it.

| Buildings - Alternative accommodation | £100,000 | |

| Buildings - Burst pipes | As standard | |

| Buildings - Escape of water excess | £450 | |

| Home emergency cover limit | £1,000 | |

| Home emergency - Central heating/boiler repair | £1,000 | |

| Buildings - Groundwater flooding | Not covered | 0 out of 5 |

| Subsidence excess | £1,000 | |

| Contents - Valuables unspecified single item limit | £2,000 | |

| Contents - Alternative accommodation | £25,000 | |

| Contents - Accidental damage | Optional extra only | |

| Contents - Guests' belongings | £3,000 | |

| Contents - Theft of contents in the open | £12,000 | |

| Contents - Damage to contents in the open | £12,000 | |

| Contents - Theft from outbuilding | £7,500 | |

| Contents - Damage to contents in an outbuilding | Up to contents sum insured | |

| Contents - Personal possessions cover single item limit | £50,000 |

Table last updated in September 2025. Next update in September 2026. We recommend checking policies before buying. See more on our scores below.

Use our customer scores to help you choose a great deal at MoneySuperMarket

Compare dealsWhich? earns commission to fund its not-for-profit mission if you buy a product

Dean Sobers, Which? home insurance expert, says:

Aviva’s standard policy – called Signature – was comfortably in the top half of our table for buildings cover, with 74%, and in the top fifth of our table for contents, with 79%. Its score qualified it as a Best Buy for its buildings cover.

It didn’t quite make the cut with its contents cover because of a lower-than-average acceptance rate for claims on contents-only policies.

It offers a generous £3,000 benefit for cash in the home, and has a comparatively high limit of £100,000 for alternative accommodation under its buildings cover. As the name suggests, this is the total amount available for rental costs if your home is uninhabitable during the claim and you need to live elsewhere.

The cover isn’t perfect across the board, however. For example, its contents cover doesn’t include digital downloads, which most policies now do. It also has a slightly steep excess for escape of water (water damage caused by broken plumbing), at £450.

If you have car insurance, no-claims discounts will be familiar to you – and with them no-claims discount protection (NCDP). Put simply, NCDP is an add-on that reduces the effect of making claims on your renewal premium.

NCDP is much rarer in home insurance – with Aviva’s products among one in 10 that offer it. Aviva’s add-on shields your discount for up to two claims over a three-year period.

While Signature is only available directly from Aviva, it offers Online and Premium through comparison websites.

Premium is the more comprehensive of the two. Earning scores of 74% for buildings and 70% for contents, it’s a buildings Best Buy.

Online was slightly less impressive. It was around average for buildings, with 72%, but in the bottom half of our table for its contents cover.

We asked Aviva customers who have recently made a claim how they felt about their home insurance.

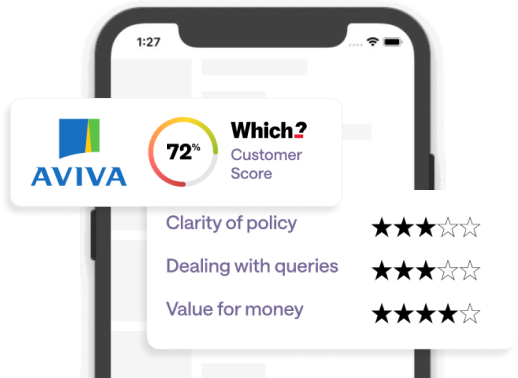

Aviva received a customer score of 72% – 6th out of 17 providers rated.

Customers were also asked to rate their most recent claim. Here, Aviva received a score of 70% – joint 5th of the 24 providers we scored. See the list of results here.

When asked why they'd rated Aviva highly, a customer praised the 'great service', while another said their policy was 'easy to understand and clear'.

| How comprehensive the policy cover is | |

| How affordable the policies are | |

| How thorough the application process is | |

| Clarity of policy | |

| Dealing with queries | |

| Fair treatment of long-standing customers | |

| Dealing with complaints | |

| Value for money |

Table last updated in September 2025. Next update in September 2026.

A dash '-' represents where we have insufficient sample size (less than 30) to generate a star rating.

Aviva sample size: customer score, 424; claims score, 516

You'll get a discount for buying combined cover rather than buying your buildings or contents insurance separately.

Aviva's Signature policy is only available direct. Its Online and Premium policies are available on these price comparison websites:

Want to pay monthly? Aviva doesn't charge interest on its Online and Signature policies. But it does charge variable interest on its Premium policy, so you might be better off paying annually on an interest-free credit card.

The above information is correct as of August 2025. For more ways to save money when buying insurance, see our guide to cheap home insurance.

With a customer score of 72%, Aviva came below just Which? Recommended Provider Tesco (75%) and Axa (73%) in our table.

Its buildings cover for its standard Signature policy scored 74% – the same score as standard policies from the Bank of Scotland, Halifax, Lloyds and Sagic. LV's standard policy was just ahead in our table, with 76%.

As for contents insurance, Aviva's standard Signature policy scored 79% and sits in 3rd place among standard policies. The standard policy from M&S Bank scored slightly higher, with 80%.

The contact number to make a claim is 0345 030 6945.

If you need to contact Aviva about a home emergency cover claim, call 0345 300 3346.

If your priority is cover for your home itself, rather than the things in it, Aviva meets our Best Buy standards and is well worth considering if the price matches your budget.

However, our verdict on its contents cover isn't quite as glowing. Although Aviva is highly rated for customer satisfaction and its contents cover looks great on paper, it has lower-than-average claims acceptance rates for contents-only policies.

This article uses insights from the Which? Connect panel, collected from research activities with our members. Find out how to get involved

Find the right policy for your home using the service provided by MoneySuperMarket

Get a quote now