By clicking a retailer link you consent to third-party cookies that track your onward journey. This enables W? to receive an affiliate commission if you make a purchase, which supports our mission to be the UK's consumer champion.

Best car insurance companies in the UK 2026

We surveyed 3,464 car insurance customers to discover the best car insurance companies and policies in the UK

Best UK car insurance companies and policies compared

Want the best car insurance policy or insurer? Use our tables below, then go to MoneySuperMarket, another comparison site or direct to the insurer.

Want the cheapest car insurance policy or insurer? Follow the links to MoneySuperMarket, or another comparison site, to get a list of policies. Then check what the policies scored by searching our tables.

The first table compares policies, ranked by policy score, and the second table compares insurance companies, ranked by customer scores.

Please note that this article is for information purposes only and does not constitute advice. Please refer to the particular terms and conditions of an insurer before committing to any financial products.

Table note: Last updated in January 2026. Next update in January 2027. Customer survey: Based on an online survey of 3,464 members of the general public who had made a claim in the past two years. Survey conducted in November 2025. Sample sizes given in 'How we analyse car insurers'. Customer score reflects the general satisfaction of customers with their insurer and their likelihood of recommending it. Claims score shows customer satisfaction with how well their most recent claim was handled and how likely they are to recommend the insurer.

If a brand isn't listed in our tables, it means it wasn't reviewed. This is either because it didn't take part in our provider survey or we weren't able to survey enough of its customers to rate its service.

Best UK car insurance

We compared 25 car insurance providers, examining the cover in their policies and analysing feedback from thousands of claimants.

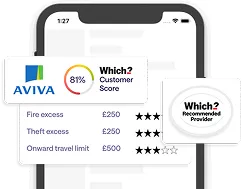

This year, Aviva was our sole Which? Recommended Provider. Claimants found it to be both affordable and to offer comprehensive cover. If your car is damaged by a pothole, you can claim without sacrificing your no-claims discount.

LV's policy was our third-highest rated. It offers a guarantee on its repairs for as long as the policyholder continues owning the car, and protection for no-claims discounts against an unlimited number of claims.

According to the latest figures from the Association of British Insurers (ABI), the average private motor insurance premium was £560 in January to March 2026 (based on premiums actually paid, rather than quotes).

That's down £20 (-3%) on the average premium of £580 in the same period in 2025.

This is good news, but follows an extended period where premiums rose, which the ABI attributes to higher vehicle repair costs and lengthier repair times. These pressures aren't ebbing. The average accidental damage claim in Jan-March was £3,699 - 8% higher than in October-December 2025.

The ABI's figure gives a good overall sense of whether car insurance premiums are rising or falling. But, in practice, the price you pay will be strongly influenced by factors such as age and location.

Car insurance premiums by age

We've worked with our price comparison partner, MoneySupermarket, to analyse how much you can expect to pay at different ages and in different regions of the UK.

Car insurance is most expensive for young drivers. They tend to have less driving experience than older drivers, and so have a greater risk of being involved in an accident and needing to make a claim.

Above the age of 70, premiums start to climb again to account for the increased risk of older drivers making more, and more expensive, claims.

Source: MoneySuperMarket. Based on average annual premiums for car insurance policies sold through MoneySuperMarket between 01/01/2026 and 0/07/2026, covering full UK car licence holders, with a minimum of 100 sales.

Car insurance premiums by region

Where you live can have a big impact on the price you pay for car insurance. City dwellers, for example, typically pay more than those living in rural areas to account for the increased risk of heavy traffic resulting in an accident and, often, higher crime rates.

This goes some way to explaining why Londoners pay, on average, more than £200 more for their annual car insurance than those living in other regions of the UK.

Region

Average annual premium

South West

£565

Wales

£602

Scotland

£634

South East

£656

North East

£674

East Midlands

£694

East of England

£701

Yorkshire and The Humber

£778

North West

£785

Northern Ireland

£827

West Midlands

£839

London

£1,064

Source: MoneySuperMarket. Based on average annual premiums for car insurance policies sold through MoneySuperMarket between 01/01/2026 and 0/07/2026, covering full UK car licence holders, with a minimum of 100 sales.

Are the best car insurance providers always the most expensive?

Our research reveals substantial differences between companies and policies in their standards of service and levels of cover.

However, this doesn't necessarily mean you'll have to pay through the nose for worthwhile cover or that a steep price means you're getting the best.

Insurers set you an individual price to reflect how they see your risk. If one insurer views you as risky or just doesn't want to compete for your custom, then even its lowest offers are likely to be pricier than policies from other providers, which could also provide much better cover.

'Is your insurer's renewal offer genuinely competitive?'

Dean Sobers, Which? car insurance expert, says:

If your experience with car insurance has been anything like that of the average driver, you'll probably have seen your premium dip – or at least level off – at last renewal, after several years of unwelcome price hikes.

Don’t confuse this for generosity on the part of your particular insurer. It’s reflective of a general trend in premiums, which means you may still be able to find better offers – and potentially better cover – elsewhere.

We think that every renewal is a great time to evaluate how competitive your insurer really is. And it’s easy to do – just run a quick quote on a comparison website (or several) to see what your insurer’s rivals are willing to offer you, and check our tables (above) to see how your policy and your insurer stack up against others.

Car insurance FAQs

Pay-per-mile car insurance is a type of insurance where you pay a lower-than-normal baseline premium, and make an extra payment for each mile you drive.

It's a form of black box (telematics) insurance, which only records your mileage and not other aspects of your driving behaviour.

It's worth considering if your mileage drops off considerably as you get older – for example, if you retire and no longer need to commute. As a rule of thumb, if you drive less than 6,000 miles a year, pay-per-mile car insurance may work out cheaper than a standard policy.

If you have a comprehensive car insurance policy, then it will typically cover vandalism.

However, if you need to make a vandalism claim, you will usually have to pay an excess. It may also affect your no-claims bonus.

This is because vandalism is considered a 'fault' claim because your insurer won't be able to recover costs from the vandal.

From haggling with your provider to using comparison sites, there are many ways to find cheap car insurance. Shop around and do your research to understand what a competitive price looks like before making a decision.

Insurance companies are no longer allowed to offer better deals to new customers, so it is in your best interest to find out what your current provider is willing to offer as well as checking out the best deals on price comparison sites.

To see the full range of policies available, you'll need to work a bit harder than running quotes on comparison websites. Some insurers don't make all their policies available through them, while others - such as NFU Mutual - aren't online at all and only do business over the phone.

From January to March 2026, the average annual premium paid by drivers was £560, according to the Association of British Insurers - equating to £47 a month.

Your excess, car model type and your age can increase your premiums.

Bear in mind that spreading payments monthly, rather than paying for a year in one go, can cost you more. We've seen cases of insurers charging over 30% interest - similar to a bank overdraft.

An excess is the amount you pay towards any claim you make on your car insurance policy. For example, if you have a claim worth £500, and a £100 excess, you'll only receive £400 from your insurer.

Most car insurers have two types of excess: a compulsory excess, which can't be modified; and a voluntary excess, which you can set yourself.

Set your voluntary excess carefully. Your insurer will offer you a lower premium if you opt for a higher excess, but you'll be committing to paying more if you claim. Where damage to your car has been minor, a high excess can mean it's not worth claiming at all.

The simplest way to find out if your car is insured is to use the Motor Insurance Bureau, which is a national register of all cars insured in the UK.

Enter your vehicle's registration number, confirm ownership, and receive a quick response indicating your insurance status. Keep in mind that updates could take some time if you have recently purchased insurance coverage.

Beware of potential scam callers claiming to be from the Motor Insurance Bureau (MIB) and avoid sharing personal information over the phone.

Yes. Your car insurer will automatically provide third-party cover (the legally required minimum) if you're driving in the European Economic Area.

However, you may need a green card to prove that you have valid cover, depending on the country you're driving in. At the time of writing, you don't need a green card to prove your insurance cover if driving in the EU (including Ireland), Andorra, Bosnia and Herzegovina, Iceland, Liechtenstein, Montenegro, Norway, Serbia and Switzerland.

You can find out which countries you need a green card to drive in on gov.uk.

It's recommended that you contact your insurer about a month ahead of travel to ensure the green card reaches you in time.

If you don't have a green card in a country where one is required, you'll have to buy insurance locally. This may be more expensive than UK cover.

Key information

Comprehensive cover overseas

Some insurers throw in more than just the legal minimum, extending comprehensive cover for a limited time overseas.

This allowance period can vary between insurers from a long weekend to a whole year's worth – 60 to 90 days is fairly common. Once that period elapses, your cover reverts to the basic legal level.

Some insurers let you extend the allowance period. You can do this when you take out the policy or request an extension if you plan a trip. It's best to give your insurer as much notice as possible.

Yes, accumulating three points on your driving licence can significantly increase your car insurance premiums.

Insurance companies typically see penalty points as signs of risky driving behaviour, which increases the likelihood of future claims, so they adjust premiums accordingly to reflect this increased risk.

If your insurance quotes are high due to penalty points, you could consider comparing insurance quotes, exploring policy options like black box cover, or negotiating with insurers to potentially help bring the quotes down.

Yes. It's standard for your agreement to auto-renew after 12 months - however, we would suggest that you don't let your car insurance policy auto-renew, as you could be losing hundreds by not shopping around.

When it comes to auto-renewal, your provider will let you know between 21 and 30 days prior that your policy is up for renewal, and if you take no action it will auto-renew with the same details including excess, no-claims bonus, add-ons, fees and charges.

Some policies have a 10-month option, so check your agreement to see how many months until your auto-renew kicks in.

Don't just renew - your existing insurer may not be the cheapest option, especially if you haven't switched for a while.

Start with price comparison sites but bear in mind not all insurers or policies are on them. Also make sure the price comparison site is listing your details (such as profession) correctly.

If you've got a complicated claims history you could use a broker to find cover, through the British Insurance Brokers Association. Watch out for fraudulent 'ghost brokers', particularly on social media; these claim to offer cut price cover but leave you with little or no insurance.

Black box: consider black box insurance, which adjusts premiums based on driving habits. Opt for a car with a small engine, avoid modifications, and drive less to reduce risk. Adding an experienced driver might help, but don't 'front' (adding another driver as the main driver when you really do most of the driving) as this is against the law. Compare quotes and consider raising the excess. While black box insurance offers fair pricing, make sure you understand the rules and penalties for bad driving - how black box car insurance works.

Learner driver insurance: you could consider learner driver insurance if you're practicing in your own or someone else's car to help cut costs. Choose between a dedicated learner driver policy or being added as a named driver. Compare quotes, opt for insurers with restrictions, increase voluntary excess, and consider comprehensive coverage as it might be cheaper. Temporary learner driver insurance is available for shorter practice periods. Additionally, shop around, as rates vary widely among insurers - see our guide on learner driver insurance.

Younger drivers could also benefit from multi-car insurance.

Your 50s and 60s should be among your cheapest years for car insurance, as long as you choose the right policy.

However, as you age, expenses may start to rise, and some insurers could refuse to provide coverage altogether.

Whilst specialist over-50s policies exist for older drivers, they may still find that standard insurers are cheaper. Make the most of your no-claims discount, which can be eroded by rising premiums, and if switching, check your new insurer will recognise it.

Yes. Your policy can be transferred to your new car even if you are midway through your 12-month policy. Once the transfer is complete, your new car will be covered in the same way as your previous model.

Some providers will charge an admin fee to change your details. These changes should include your car make, model and mileage. Your new car could have an impact on your insurance premiums.

Your provider will need to know the date to switch over the policies. The best time to contact it is once you know when you are collecting your new car from the dealership or seller. This way, you can collect your car and drive it home that day with your new insurance applied.

If you're added to another driver's policy – listed as a 'named driver' – then you will be covered to drive their car up to that policy's level of cover.

Your policy may also have some cover for driving cars (known as 'driving other cars' cover or 'DOC') even where you aren't named on the owner's policy.

However, DOC cover usually only provides third-party cover and, in many policies, only applies if you're making use of the car in an emergency situation.

If your car is being driven, it can't be sold without insurance.

Your car can be sold if it has been declared off-road (known as SORN - Statutory Off Road Notification) - but it still must be insured and taxed before it can be driven on a public road.

This would include if it was being driven to transfer to the buyer.

No. Car insurance is designed to cover damage to cars, people and property as a result of an accident.

As standard, your main car insurance policy won't cover mechanical breakdowns or engine failures.

Some car insurance policies offer vehicle breakdown assistance cover as an optional extra (NFU Mutual offers it as standard), or you can buy standalone breakdown cover.

If you have a comprehensive car insurance policy, then it will typically cover vandalism.

However, if you need to make a vandalism claim, you will usually have to pay an excess. It may also affect your no-claims bonus.

This is because vandalism is considered a 'fault' claim because your insurer won't be able to recover costs from the vandal.

It depends on the reason for the damage. Car insurance can cover the cost of repairing scratches and dents following an accident or vandalism, but it won't cover the cost of cosmetic scratches from gravel thrown up while driving, for example.

However, even if the scratch or dent is covered, it may not be worth claiming. This is because the cost of any excess may exceed the cost of paying for a repair yourself, and making a claim could affect your no-claims bonus.

As with banking customers, insurance policyholders in the UK benefit from the protection of the Financial Services Compensation Scheme (FSCS) if their insurer goes bust. This means:

If you're entitled to a refund of some of your premium, the FSCS will repay 90% of the owed amount.

If someone has made a claim against you that's covered by your insurance, the FSCS will pay it in full.

If you have an outstanding claim with your insurer that it can no longer pay, the FSCS will pay 90% of it.

How we analyse car insurance

Our editorial independence means we can work on behalf of consumers, not insurers. That means our reviews are fair and there's no hidden agenda.

Customer and claims scores

This is based on a survey of 3,464 policyholders who have recently made a car insurance claim. The customer score reflects how satisfied customers are with their provider and, where they're still with that insurer, how likely they would be to recommend it. Claims score shows customer satisfaction with how well their most recent claim was handled and how likely they are to recommend the insurer.

Insurers must receive a minimum of 40 customer responses to be included.

Customer score/claims score sample sizes:1st Central (58/72), AA (441/513), Admiral (402/491),Allianz (57/88), Aviva (598/680), Axa (303/366), Churchill (117/150), Direct Line (170/198), Esure (na/40), Hastings Direct (97/127), Lloyds Bank (na/52), LV (80/109), RAC (44/46), Tesco (54/74).

Why only talk to customers who've claimed?

You'll only know how good an insurer's customer service is when you make a claim.

That's when good insurers will show their ability to deal with problems, quickly process your claim and get you back on the road as soon as possible.

As it can be difficult to find the requisite number of customers who have claimed for some insurers, in some cases we're only able to provide our expert policy scores.

Policy score

This is our assessment of the quality of standard cover, comparing 94 elements of a policy. We weight certain features of cover or costs (fees and excesses) based on the impact we think they generally make, from courtesy cars to replacement keys.

Among the highest-weighted elements are the insurer's guarantee on repairs, cover for glass damage, conditions of its no-claims discount, whether it will provide a replacement vehicle, fire, theft and accidental damage excesses, and interest rates charged for paying premiums in instalments.

We carry this analysis out every year. The next update will be in January 2027.

We review a lot of policies – and our 'Best Buy' badge recognises the individual products that stood out as being the most comprehensive in our analysis. It doesn't reflect customer service. However, we won't give a provider a Best Buy badge where there's evidence – either from our surveys or from Financial Conduct Authority data – of poor service or a poorer-than-average record of paying claims.

Policies named as Best Buys must have a minimum policy score of 65%.

Additionally, we look at how consistently good the cover is in policies. To make the cut, a policy needs to have scored at least three out of five points in two thirds of the areas we've rated (see 'policy scores' for more).

Last, all Best Buy policies must provide – either as standard or as an option – the following levels of cover as a minimum:

Comprehensive cover (meaning it covers third-party claims, fire, theft and accidental damage to your car), a temporary courtesy car if yours is under repair or if it has been stolen or written off, a repairs guarantee period of at least three years, cover for damage to your windows or windscreen, legal expenses cover, liability cover of £20m or more and personal accident cover.

More questions on car insurance? Take a look at our guides: